By RP Staff, on Mon Aug 8, 2011 at 4:15 PM ET The RP is currently holding forth on Wall Street Journal Radio — the Daily Wrap with Michael Castner — about today’s economic crisis and his nationally-discussed piece, Credit Downgrade for Dummies.

To listen to the program live, click here, or on the logo below:

By RP Staff, on Mon Aug 8, 2011 at 3:30 PM ET The RP wil be interviewed this afternoon at 4:15 PM EDT on Wall Street Journal Radio about today’s economic crisis and his nationally-discussed piece, Credit Downgrade for Dummies.

To find out what radio affiliate carries the show in your area, click here.

To listen to the program live, click here.

By RP Staff, on Mon Aug 8, 2011 at 12:00 PM ET Just as Jerry Lewis is to France, the RP is to Canada — the inexplicable expert on all matters of the American economy. Over the weekend, CTV, Canada’s CNN, interviewed the RP about the impact of the S&P credit downgrade.

Click here, or on the logo below, to watch:

By RP Staff, on Mon Aug 8, 2011 at 8:30 AM ET In case you were battling the heat and rain of Kentucky’s Fancy Farm political festivities — or more appropriately, were enjoying some quality time with your family — you may have missed the RP’s latest column that The Huffington Post touted on its home page all weekend.

Having received positive feedback — and considerable media attention — from his piece two weeks ago,”Debt Ceiling for Dummies,” the RP penned a column to help explain in similarly straight-forward terms the import of Friday night’s decision by S&P to downgrade U.S. credit.

Here’s an excerpt from “Credit Downgrade for Dummies“:

Why should we listen to the credit agencies — aren’t they part of the problem?

There is broad consensus that credit rating agency action — or often times, inaction — was a significant contributor to the 2008 financial collapse. This April, a U.S. Senate investigations panel declared that Moody’s and S&P triggered the financial crisis when they were forced to downgrade their ratings on the very complex and controversial mortgage-backed securities that were at the heart of the collapse that almost brought our entire financial system to its knees. Had the ratings agencies been exercising more diligence, many experts argue, they would have alerted investors of the riskiness of these controversial financial instruments long before they became a problem.

However, while the credit ratings agencies do not enter the discussion with entirely clean hands, their decisions are extraordinary significant. Their role is written into the statutes and regulations that govern the financial system. Think of it this way: Even though progressives may decry the partisanship on the U.S. Supreme Court, and thoroughly detest some of its recent 5-4 decisions, we must abide by them.

Click here to read the RP’s full piece, “Credit Downgrade for Dummies” at The Huffington Post.

By Jonathan Miller, on Sat Aug 6, 2011 at 2:30 PM ET Having received positive feedback — and considerable media attention — from my piece two weeks ago that explained the sometimes esoteric, often confusing subject matter surrounding the debt crisis debate (“Debt Ceiling for Dummies“), I decided today to pen a quick column to help explain in similarly straight-forward terms the import of last night’s decision by S&P to downgrade U.S. credit.

Here’s an excerpt from my latest Huffington Post column, “Credit Downgrade for Dummies“:

Who are the credit rating agencies and what did they just do?

There are three primary national credit rating agencies: Fitch, Moody’s Investors Service (“Moody’s”), and Standard and Poor’s (“S&P”). These agencies rate the creditworthiness of governments, companies and individual securities, allowing investors to better understand the risk of their investments. The higher the rating, the more creditworthy — or, alternatively, the less risky — the investment.

Our federal government is one of the many entities these agencies rate. The U.S. borrows money — by issuing bonds and Treasury bills to governments, corporations and individual investors — in order to operate all of its essential functions. The outstanding current federal debt currently exceeds $14.5 trillion.

Since the credit rating agencies were established, U.S. Treasuries have always enjoyed a triple A rating, the very highest: indicating to global financial markets that they are among the safest investment instruments in the world. Friday night, however — for the first time in the nation’s history — S&P downgraded the rating of the nation’s long-term debt to AA+, one notch below AAA, meaning that the U.S. has been removed from its list of risk-free borrowers.

Earlier in the week, Moody’s and Fitch both declined to downgrade the country’s credit rating. Moody’s, however, changed its “outlook” on U.S. debt to “negative,” meaning that there is a risk of a future downgrade. Fitch stated it would determine whether to lower its own outlook by the end of the month. Both have urged Congress to make more progress in debt reduction in order to avoid a potential full downgrade.

Click here to read my full piece, “Credit Downgrade for Dummies” at The Huffington Post.

By Grant Smith, RP Staff, on Fri Aug 5, 2011 at 3:00 PM ET

The real reason why stocks are tanking. [Fortune]

Three stocks to buy as the market tanks. [TheStreet.com]

Congress reaches a deal on the Federal Aviation Administration shut-down. [Washington Post]

Couple arrested for selling bongs at a county fair in Pennsylvania. [CBS]

By Rod Jetton, on Fri Aug 5, 2011 at 8:30 AM ET Contributing RP Rod Jetton has launched his own blog to comment on Missouri politics. Here is his first entry:

_Marble_Hill") There was a lot of talk about tax credits in the last legislative session. I would like to recommend one tax credit that would only cost a maximum of 2 million per a year, but will help thousands of Missourians get enough to eat. It’s the Local Food Pantry Tax Credit Program (LFPTCP) that was started in 2008 and is scheduled to expire in 2012. The Oversight Division of the Joint Committee on Legislative Research issued a report showing that the first three years of the four-year program, only $1.5 million of the $6 million available credits were claimed, but use has grown significantly each year, with nearly $800,000 claimed in 2010. The average donation was $450 with 99 percent of the statewide credits being claimed by individual taxpayers.

While the battle rages in Jefferson City about how to reform our tax credit programs. This program already includes many of the reforms that have been debated. Most tax credit reformers have four main goals, which include:

1. Cap the amount of tax credits one individual can receive 2. Keep tax credits from being sold or transferred

3. Cap the overall amount that can be spent on any one program.

4. Sunset all tax credit program

By Michael Steele, on Thu Aug 4, 2011 at 8:30 AM ET  I, like many of you, probably spent more time than I really wanted watching political “leaders” in Washington free-fall to a decision on our nation’s debt. As I listened to the partisan excuses, whines and outright misrepresentation of what triggers a “default,” it occurred to me that all of the drama and general posturing by both Democrats and Republicans over raising the nation’s debt ceiling could have been avoided. I, like many of you, probably spent more time than I really wanted watching political “leaders” in Washington free-fall to a decision on our nation’s debt. As I listened to the partisan excuses, whines and outright misrepresentation of what triggers a “default,” it occurred to me that all of the drama and general posturing by both Democrats and Republicans over raising the nation’s debt ceiling could have been avoided.

When asked on Dec. 8, 2010, whether he and the other Democrats would raise the debt ceiling, Senate Majority Leader Harry Reid responded, “Let the Republicans have some buy-in on the debt. They’re going to have a majority in the House. I don’t think it should be [done] when we have a heavily Democratic Senate, heavily Democratic House and a Democratic president.”

So as I watched members of Congress, especially Sen. Reid, looking sullen and complaining about the Tea Party caucus in the House and the “intransigence of Republicans” overall throughout the debt-ceiling talks, I thought back to that Dec. 8 interview and wondered what we would be talking about right now if the Democrat majorities in the House and Senate (under the leadership of the White House) had passed an increase in the debt ceiling in December. Perhaps we’d be talking about jobs?

It is no wonder, then, that this proud nation and its hardworking citizens found themselves on the brink of financial default and bankruptcy because some in Washington would rather play “gotcha” politics with our problems than solve them.

A Federal Fiscal Crisis

And yet we can no longer afford to deny what we already know: Federal spending has spun out of control, surging 47 percent between 2001 and 2008, with spending increasing 9.1 percent (or $249 billion) in 2008 (the last year of President George Bush’s term) and now reaching a whopping 30 percent of the gross domestic product after the first two years of the Obama administration. Annual entitlement-program spending accounts for 54 percent of the nation’s budget, and these fixed costs have soared by 6.4 percent since 2000.

Read the rest of…

Michael Steele: Debt Deal Is Not About Who Won and Lost

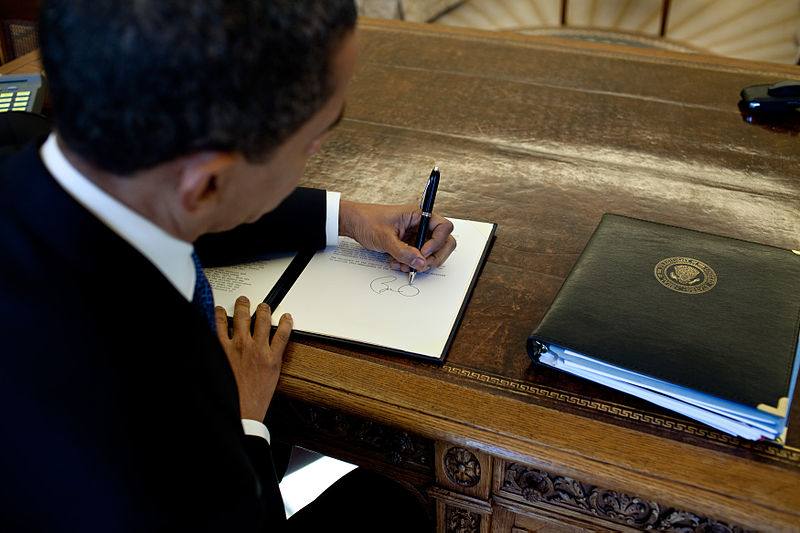

By Patrick Derocher, on Tue Aug 2, 2011 at 4:04 PM ET Ending weeks of highly contentions debate, President Obama signed the Budget Control Bill into law on Monday afternoon. The long national nightmare, as Gerald Ford might say, is over. After the Budget Control Bill sailed to approval in the Senate, garnering 74 “Ayes” and 26 “Noes,” President Obama signed the compromise he brokered with Senate Minority Leader Mitch McConnell of Kentucky. The bill had previously passed in the House of Representatives by a margin of more than 100: 269 “Ayes” to 161 “Noes.” [Politico]

Now that the Bill has been signed into law, the question has been raised as to who will sit on the 12-member “Super Congress” to determine the eventual cuts that will be made to bring the deficit reduction to $2.1 trillion. Provisions have been made for each majority and minority leader to appoint three individuals. Names being tossed around by the punditry include Republicans John Kyl, Mike Crapo, and Paul Ryan, and Democrats Dick Durbin, Max Baucus, and Kent Conrad. [Washington Post]

Somewhat ironically, the budget reduction committee will come with an as-of-yet-undetermined, potentially very high, costs that are just beginning to be worked out. The costs will have to be determined shortly, as the new law requires it be convened within 45 days of the passage- today. [Roll Call]

The 2012 Republican candidates are using the passage of a debt deal as a soap box of sorts from which to discuss their views on the debt and deficit. Only former Utah governor Jon Huntsman has come out fully in support of the bill (though he referred to it as less-than-ideal), while Michele Bachmann, Ron Paul, Tim Pawlenty, and most recently Mitt Romney have come out in opposition to the deal, saying it does not go far enough. Meanwhile, Texas Governor Rick Perry, who has not entered the race but is widely speculated to be a late entrant, has kept completely silent on the matter. [Daily Caller]

Fitch has said that, even if the United States retains its AAA rating, the agency may well downgrade the country’s outlook to negative when it finishes ratings reviews at the end of August. [Reuters]

By RP Staff, on Tue Aug 2, 2011 at 2:30 PM ET From 2:30 PM to 3:00 PM EDT, the RP will be the guest on Bloomberg Radio, to discuss the debt ceiling crisis and all of the latest developments.

Click here, or on the logo below, to listen to the interview LIVE online.

|

The Recovering Politician Bookstore

|

_Marble_Hill")

{kind=link}

{kind=link}